How to Check if a Contractor Is Insured in Ontario

Insurance, WSIB, and bonding explained for homeowners

Before hiring someone to work in your home, there’s one question that matters more than most:

Are they properly covered?

It’s easy to focus on price, availability, or even personality. But if something goes wrong and the contractor isn’t insured or covered by WSIB, the situation can become much more complicated than expected.

This is especially true in Ontario, where many small operators work independently, sometimes without full coverage or documentation.

This guide walks you through how to check if a contractor is insured in Ontario, and what to look for when it comes to WSIB and bonding.

Why this matters more than people think

When someone works in your home, a few things can go wrong:

- A worker gets injured

- Property is damaged

- A subcontractor is brought in without proper coverage

- A job is left incomplete

If the contractor is properly insured and registered, these risks are managed.

If not, you may be exposed to liability, delays, or out-of-pocket costs.

Most homeowners don’t realize this until it’s too late.

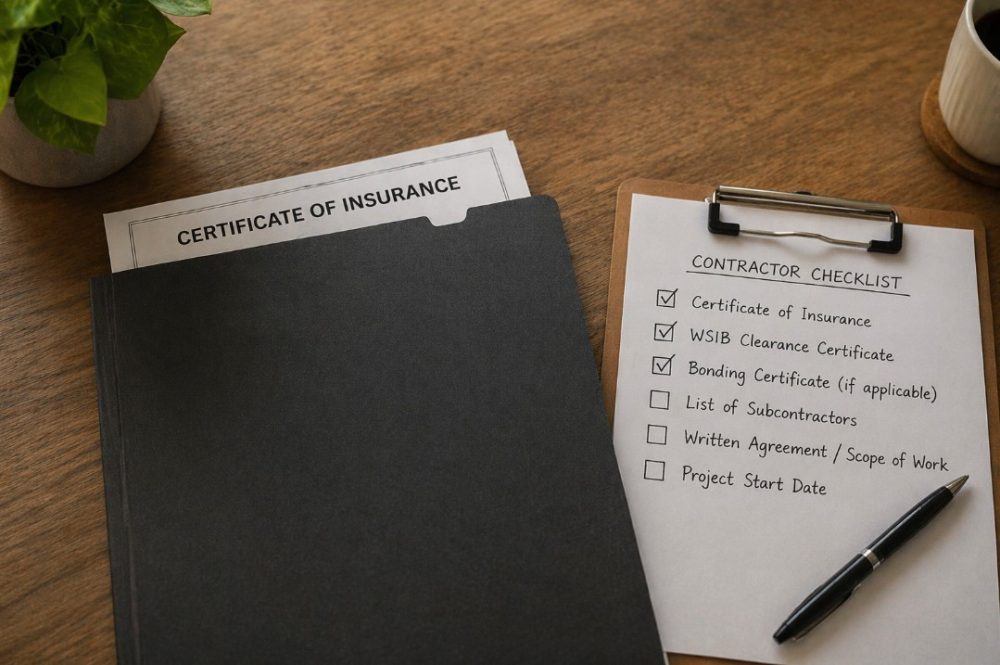

Step 1: Ask for a certificate of insurance

The first and most important step is simple:

Ask for a certificate of insurance.

This document confirms that the contractor carries liability insurance (often called commercial general liability or CGL).

What to look for:

- Valid policy dates

- Name of the insured business

- Coverage limits (typically $1M–$2M or more)

- Description of operations (e.g. handyman, renovations, installations)

Why it matters:

If something is damaged in your home or someone is injured, this policy is what protects both you and the contractor.

Without it, you may be relying on your own homeowner’s insurance or dealing with legal recovery.

Step 2: Verify WSIB coverage (this is often overlooked)

In Ontario, WSIB (Workplace Safety and Insurance Board) provides coverage for workers who are injured on the job.

If a contractor has employees or uses subcontractors, WSIB coverage is often required.

What to ask for:

- A WSIB clearance certificate

This confirms the contractor’s account is in good standing.

Why it matters:

If a worker is injured on your property and there is no WSIB coverage, liability can become complicated very quickly.

Important nuance:

Some independent operators (working alone on private homes) may be exempt.

But:

- The moment they bring in help

- Or take on broader work

WSIB expectations change.

A professional contractor will be able to explain their status clearly.

Step 3: Ask if the contractor is bonded

Bonding is less common for small jobs, but still worth asking about.

A bond is a form of protection that covers you if:

- The contractor doesn’t complete the work

- The work fails inspection

- Funds are taken and the job is abandoned

What to ask:

- “Are you bonded?”

- “Can you provide a bond certificate if needed?”

Why it matters:

It adds another layer of accountability, especially for larger or multi-stage projects.

Step 4: Ask about subcontractors

Even if the person you hire seems fully covered, the real risk often comes from who they bring in.

Ask:

- Do you use subcontractors?

- Are they insured?

- Do they have WSIB clearance?

In practice, this is where things can break down.

Uninsured subcontractors are not uncommon, and if something happens, it can affect both you and the primary contractor.

Step 5: Get it in writing

Before any work begins, make sure you have:

- A written agreement

- Clear scope of work

- Confirmation of who is doing the work

- Documentation of insurance and WSIB where applicable

This does not need to be complicated.

But it should be clear.

A simple checklist you can use

Before hiring a contractor in Ontario, confirm:

- Certificate of insurance (valid and current)

- WSIB clearance certificate (if applicable)

- Bonding (for larger jobs)

- Subcontractor coverage

- Written agreement

If someone hesitates to provide these, that’s usually a sign to pause.

A better way to approach hiring

Hiring help for your home should reduce stress, not add to it.

The reality is that many homeowners don’t know what to ask, and many providers don’t volunteer this information.

That’s where problems start.

At Good Company, we take a straightforward approach:

- Fully insured

- WSIB-covered

- Documentation available on request

- Same expectations for any subcontractors we bring in

We believe this should be standard, not a selling point.

Final thought

If you remember one thing, let it be this:

It’s not awkward to ask for proof. It’s responsible.

A professional contractor will expect the question and respect it.

And taking a few minutes to check now can save you a lot of trouble later.